H2H Battle - Loblaw vs. Metro

Enjoy a spirited clash between two industry competitors, pitted against carefully chosen financial metrics and benchmarks.

The Canadian grocery and retail pharmacy industry is a mature, highly competitive market characterized by stable demand for essential goods and services. It encompasses supermarkets, discount grocers, specialty food stores, and pharmacies, serving a population of approximately 40 million. Dominated by a few large players, it is concentrated in urban centers like Ontario, Québec, and British Columbia, though rural and regional markets remain significant. Key trends shaping the industry include the rise of e-commerce, increasing consumer demand for private-label products, and a focus on health and wellness offerings. The sector is considered defensive, as food and pharmaceuticals are recession-resistant staples, though it faces pressures from slim margins, price competition, and evolving consumer behaviors.

Metro and Loblaw are two of Canada’s "Big Three" grocers, alongside Sobeys, collectively controlling over 60% of the grocery market. Loblaw is the largest player, with a national presence, while Metro has a stronghold in Québec and Ontario. Both companies have expanded into pharmacies—Loblaw through Shoppers Drug Mart and Metro via Jean Coutu—broadening their revenue streams and enhancing customer retention through integrated loyalty programs.

Key Competitors

Loblaw Companies Limited (L.TO): Canada’s largest grocer and pharmacy retailer, operating banners like Loblaws, No Frills, Real Canadian Superstore, and Shoppers Drug Mart. Its scale, loyalty program (PC Optimum), and private-label strength (President’s Choice) make it a dominant force.

Metro Inc. (MRU.TO): Third-largest grocer with a focus on Québec and Ontario, operating Metro, Super C, Food Basics, and Jean Coutu pharmacies. Known for regional dominance and private-label offerings (Irresistibles, Selection).

Sobeys Inc. (owned by Empire Company Limited, EMP.A.TO): Second-largest grocer, with a national presence through Sobeys, Safeway, FreshCo, and IGA. Competes via competitive pricing and a strong presence in Atlantic Canada and Western provinces.

Walmart Canada (WMT): A major international player offering groceries at low prices through supercenters and discount stores, appealing to cost-conscious consumers with one-stop shopping.

Costco Wholesale Canada (COST): Operates a membership-based warehouse model, providing bulk groceries and household goods at competitive prices, targeting value-driven shoppers.

Dollarama Inc. (DOL.TO): A discount retailer overlapping with grocery through low-cost packaged foods and household items, competing for budget-conscious consumers.

Headwinds

Intense Price Competition: With slim margins (typically 2-4% net), grocers face pressure from discount chains and Walmart, limiting pricing power and forcing reliance on volume over markups.

Inflation and Cost Pressures: Rising costs for food, labor, and transportation strain margins, especially if consumer resistance prevents full cost pass-through.

Regulatory Scrutiny: Allegations of price-fixing (e.g., the bread price-fixing scandal involving Loblaw and others) and growing public frustration over grocery profits amid inflation have led to calls for stricter oversight, potentially impacting operations.

E-commerce Costs: Building and maintaining online platforms and delivery infrastructure require significant investment, with profitability lagging behind physical stores due to logistics expenses.

Shifting Consumer Preferences: Demand for organic, sustainable, and local products challenges traditional supply chains, while younger consumers favor convenience over loyalty.

Tailwinds

E-commerce Expansion: The shift to online grocery shopping, accelerated by the pandemic, continues to grow.

Private-Label Strength: Rising inflation drives demand for affordable private-label products, boosting margins for companies.

Defensive Nature: As a staple goods sector, grocery and pharmacy retail benefits from consistent demand, offering stability during economic downturns or geopolitical uncertainty.

Pharmacy Growth: Aging demographics and increased healthcare spending fuel pharmacy revenue, with integrated grocery-pharmacy models enhancing cross-selling opportunities.

Operational Efficiency: Investments in automation, supply chain upgrades, and labor-saving technologies improve profitability despite rising costs.

Loblaw (L)

Company Overview

Loblaw Companies Limited is Canada’s largest food and pharmacy retailer, headquartered in Brampton, Ontario.

Founded in 1919 by Theodore Loblaw and John Milton Cork, it has grown into a dominant force in the Canadian retail landscape operating a vast network of over 2,400 corporate, franchised, and associate-owned stores across Canada, making it a household name with a coast-to-coast presence.

The company is majority-owned by George Weston Limited (WN.TO), which holds about 52% of its shares, with the Weston family maintaining significant influence.

Loblaw’s ticker, L.TO, reflects its status as a blue-chip stock, known for stability and consistent dividend growth in the defensive retail sector.

Business Model

Loblaw’s business model is built on a diversified, integrated approach to retail, leveraging scale and synergies across its operations. Key components include:

Multi-Format Retailing: Loblaw operates a range of store formats—supermarkets, discount stores, and pharmacies—tailored to different customer segments, from premium to budget-conscious shoppers.

Franchising and Associate Stores: It franchises many smaller locations (e.g., Shoppers Drug Mart, No Frills) to independent operators, reducing capital expenditure while expanding reach and sharing operational risks.

Vertical Integration: Loblaw controls significant portions of its supply chain, including distribution centers and private-label manufacturing, ensuring product availability and cost efficiency.

Pharmacy and Healthcare: The 2006 acquisition of Shoppers Drug Mart added a high-margin pharmacy business, integrating health services with grocery offerings.

Digital and Loyalty Programs: Loblaw invests heavily in e-commerce (e.g., PC Express) and its PC Optimum loyalty program, which boasts over 18 million members, driving customer retention and data-driven marketing.

Financial Services: Through President’s Choice Financial, it offers banking, insurance, and credit card services, enhancing customer engagement and generating ancillary revenue.

This diversified model positions Loblaw as a one-stop shop, capitalizing on both essential goods demand and discretionary spending.

Product and Service Offerings

Loblaw provides an extensive portfolio of products and services across its grocery, pharmacy, and ancillary divisions:

Food Retail: Offers a wide range of grocery items, including fresh produce, meats, dairy, bakery goods, frozen foods, and prepared meals. Its banners include Loblaws, Zehrs, Real Canadian Superstore, No Frills, and Maxi, catering to diverse income levels and preferences.

Private Labels: Features acclaimed brands like President’s Choice (premium foods), No Name (value-focused), and Life Brand (health products), which account for a significant portion of sales and boost margins.

Pharmacy: Through Shoppers Drug Mart and Pharmaprix (Québec), Loblaw provides prescription drugs, over-the-counter medications, beauty products, and healthcare services like vaccinations and clinics.

Specialty and Ethnic Offerings: Operates T&T Supermarkets, Canada’s largest Asian grocery chain, targeting multicultural markets with specialized products.

E-commerce: PC Express offers online grocery shopping with pickup and delivery options, integrating with physical stores for seamless service.

Apparel and General Merchandise: Joe Fresh, a private-label clothing line, and select stores offering household goods diversify revenue beyond food and pharmacy.

Financial Products: President’s Choice Financial provides no-fee banking, credit cards, and insurance, linked to the PC Optimum program for added value.

These broad offerings mix ensures Loblaw appeals to a wide customer base while maximizing cross-selling opportunities.

Competitive Position and Advantages

Loblaw holds a commanding position as Canada’s largest grocery and pharmacy retailer, with an estimated 30%+ share of the grocery market and a leading pharmacy network via Shoppers Drug Mart. Its competitive advantages include:

Scale and Market Leadership: As the biggest player, Loblaw benefits from unmatched purchasing power, enabling competitive pricing and supplier negotiations that smaller rivals like Metro struggle to match.

Diverse Store Portfolio: Its mix of premium (Loblaws), discount (No Frills), and mid-tier (Real Canadian Superstore) banners allows it to capture all consumer segments, reducing vulnerability to economic shifts.

Private-Label Dominance: President’s Choice and No Name brands are category leaders, offering high-quality, affordable options that drive loyalty and higher margins (private labels account for ~50% of sales in some categories).

Loyalty Program Strength: PC Optimum is one of Canada’s most successful loyalty programs, providing valuable consumer data and fostering repeat purchases across grocery and pharmacy.

Pharmacy Integration: Shoppers Drug Mart’s 1,300+ locations create a unique grocery-pharmacy synergy, enhancing convenience and tapping into the growing healthcare market.

National Footprint: Unlike Metro’s regional focus, Loblaw’s presence spans all provinces, giving it broader exposure and resilience against regional economic downturns.

However, its size invites scrutiny (e.g., the bread price-fixing scandal), and it faces fierce competition from discount rivals like Walmart and Costco.

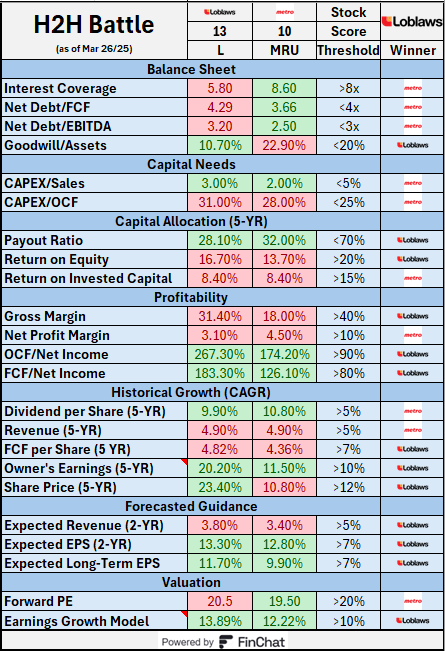

Metro still owns a significant portion of its properties, unlike Loblaw, which has largely divested its real estate holdings through Choice Properties REIT. Metro’s strategy offers stability and cost control, which are valuable in the competitive, low-margin grocery sector, but it may constrain its ability to scale rapidly. Loblaw’s divestiture has freed up capital for growth and innovation, contributing to its stronger financial performance (e.g., 23.40% share price growth over five years compared to Metro’s 10.80% as of March 2025), but it comes at the cost of higher lease expenses and less control over its physical assets.

Metro (MRU)

Company Overview

Metro Inc. is a leading Canadian company in the food and pharmaceutical retail sectors, headquartered in Montréal, Québec.

Founded in 1947, it has grown into one of Canada’s major grocery and pharmacy operators, with a significant presence primarily in Québec and Ontario.

Metro operates as a retailer, franchisor, distributor, and manufacturer, serving a broad customer base through its extensive network of stores and pharmacies. It operates under various banners, including Metro, Metro Plus, Super C, Food Basics, and Adonis for groceries, and Jean Coutu and Brunet for pharmacies.

It is publicly traded under the ticker MRU.TO, with a diverse ownership structure that includes institutional investors, the founding Montreuil family, and retail shareholders.

Business Model

Metro Inc.’s business model is multifaceted, designed to maximize efficiency and customer reach in the competitive retail landscape. It operates through several key strategies:

Retailing: Metro owns and operates supermarkets and discount stores, directly selling to consumers under banners like Metro, Metro Plus, Super C, and Food Basics.

Franchising: The company licenses its trademarks and supplies merchandise to franchisees, particularly in smaller neighborhood stores and pharmacies, enhancing its market penetration without bearing all operational costs.

Distribution: Metro leverages its supply chain capabilities to service both its own stores and smaller independent grocers, ensuring product availability and economies of scale.

Manufacturing: It produces private-label food products and generic drugs, adding value and boosting margins by controlling quality and costs.

Digital Integration: Metro offers online grocery shopping services, aligning with evolving consumer preferences for convenience.

This hybrid model allows Metro to cater to diverse customer segments while maintaining operational flexibility and profitability in a highly competitive industry.

Product and Service Offerings

Metro Inc. provides a wide range of products and services across its food and pharmaceutical divisions:

Food Retail: Offers fresh and grocery products, including meats, dairy, fruits, vegetables, frozen foods, bakery items, prepared meals, and deli products. Its private-label brands, such as Irresistibles, Selection, and Première Moisson, enhance its offerings with exclusive, cost-effective options.

Pharmacy: Through its acquisition of the Jean Coutu Group in 2018, Metro operates pharmacies under banners like Jean Coutu and Brunet, providing prescription drugs, over-the-counter medications, beauty products, and personal care items under the Personnelle brand.

Manufacturing: Produces ready-to-eat meals, salads, pastries, breads, and generic drugs under the Pro Doc trademark, strengthening its vertical integration.

Online Services: Provides e-commerce platforms for grocery shopping, including delivery and pickup options, catering to the growing demand for digital convenience.

This diverse portfolio ensures Metro meets varied consumer needs, from everyday groceries to health and wellness products.

Competitive Position and Advantages

Metro holds a strong competitive position as Canada’s third-largest grocery retailer, behind Loblaw Companies and Sobeys, and the leading pharmacy chain in Québec via Jean Coutu. Its key advantages include:

Regional Dominance: Over 70% of its operations are in Québec, where it enjoys strong brand loyalty and market share, bolstered by its pharmacy footprint.

Diverse Store Formats: From full-service supermarkets to discount stores and specialty ethnic outlets, Metro caters to a wide range of income levels and preferences.

Private Labels: Its extensive private-label offerings provide higher margins and differentiate it from competitors by offering quality at competitive prices.

Supply Chain Modernization: Recent investments, including a nearly CAD 1 billion supply chain transformation completed in 2024, enhance efficiency, product availability, and cost management.

Defensive Nature: As a grocery and pharmacy operator, Metro benefits from stable demand, making it a resilient investment during economic uncertainty.

However, Metro lacks a significant economic moat compared to larger rivals due to intense price competition and limited bargaining power with suppliers given its smaller scale.

Outcome

The grocery retail business is tightly competitive in Canada. Loblaw and Metro are the two strongest players. For growth-oriented investors, Loblaws may be the better pick due to its stronger profitability, growth, and market performance. For value or income-focused investors, Metro offers a more attractive valuation and higher dividend growth. However, it is important to note that Metro can spin off its properties to free up capital for further expansion, following the example set Loblaw.

Balance Sheet

The balance sheet metrics provide insight into the financial health and leverage of both companies. It appears Metro can cover its debt more comfortably but not drastically different. The Goodwill/Assets ratio is significantly higher for Metro. Metro carries goodwill on its books primarily due to its acquisitions of other companies, such as its purchase of Jean Coutu Group in 2018. When Metro acquired Jean Coutu, the purchase price exceeded the fair value of the acquired company's net assets, creating goodwill. In the retail/grocery industry, where margins are thin, a high goodwill percentage can be risky if those acquisitions underperform. However, to Metro’s case, this has been a strong investment.

Capital Needs

In reality, grocery retailers like Loblaws and Metro typically require consistent capital investment to maintain competitive store formats and adapt to trends like online grocery shopping. A 30% CAPEX/OCF ratio is on the high side, potentially limiting free cash flow for other uses like debt repayment or dividends.

Capital Allocation

Loblaws demonstrates slightly better capital allocation with a lower payout ratio and higher ROE, allowing it to retain more earnings for growth or deleveraging. The identical ROIC figures suggest both companies face similar challenges in generating high returns on invested capital, likely due to the capital-intensive nature of grocery retail and competitive pricing pressures.

Profitability

Loblaws shows stronger profitability metrics overall, particularly in gross margin and cash flow conversion, which are critical in the grocery sector where margins are tight. Metro's higher net profit margin is a positive, but its low gross margin suggests it may be competing more on price, which could erode profitability over time in a highly competitive market.

Historical Growth

Loblaws demonstrates stronger historical growth across most metrics, particularly in share price and owner’s earnings, suggesting better operational performance and market perception. Metro's higher dividend growth is a positive for income investors, but its overall growth profile is less robust in this competitive sector.

Forecasted Guidance

Loblaws has a slightly better growth outlook, which is a key driver of stock performance. Both companies face challenges in achieving high revenue growth due to the saturated Canadian grocery market, but their EPS growth suggests potential for profitability improvements, possibly through cost-cutting or expansion into higher-margin segments like pharmacy or e-commerce.

Valuation

Metro appears more attractively valued. However, Loblaws' higher expected return in the earnings growth model suggests the market sees more upside potential, likely due to its stronger growth and profitability metrics. In the grocery sector, where growth is modest, valuation often plays a key role, and Metro's lower P/E gives it an edge for value-focused investors.

Winner - Loblaw

Verdict - Split DecisionDisclaimer: The information provided is for educational and informational purposes only. It does not constitute financial advice or a recommendation to buy, sell, or hold any specific stocks or securities.

● Written with the help of Grok

Consider joining DiviStock Chronicles’ Referral Program for more neat rewards!

Get the H2H Battle Template for 3 successful referrals!Please refer to the details of the referral program.