H2H Battle - Railways - Canadian National vs. Canadian Pacific

Enjoy a spirited clash between two industry competitors, pitted against carefully chosen financial metrics and benchmarks.

Railroads, among the oldest forms of mechanized transport, played a pivotal role in the rise of America's "big businesses" and remain a cornerstone of global transportation infrastructure. In North America, the rail industry primarily focuses on freight transport, moving bulk commodities, intermodal containers, automotive products, and other goods over long distances. Passenger rail services, including intercity, commuter, and urban transit, also hold significant importance, especially in densely populated regions. The industry's critical role in the supply chain—transporting essential goods—underscores its stability and resilience, making it less vulnerable to economic downturns compared to other sectors.

The rail industry, however, is highly capital-intensive, requiring substantial investments in infrastructure, maintenance, and equipment. This includes constructing and maintaining tracks, purchasing locomotives and railcars, and adopting safety and technology upgrades. In North America, the rail network is highly integrated, with companies operating on standardized gauge tracks and adhering to similar standards. This integration enables the seamless interchange of railcars and locomotives between different railways, facilitating efficient transportation across regions and further enhancing the industry's operational reliability.

Key Competitors

Canadian National Railway (CNR): A leading North American freight railway operator with an extensive network across Canada and the United States.

Canadian Pacific Kansas City (CPKC): Another major North American freight railway operator, formed by the merger of Canadian Pacific Railway and Kansas City Southern.

Union Pacific (UNP): A prominent U.S. freight railway operator with a vast network across the western United States.

Norfolk Southern (NSC): A major U.S. freight railway operator serving the eastern United States.

CSX Corporation (CSX): A leading U.S. freight railway operator with a focus on the eastern United States.

BNSF Railway: One of the largest freight railway operators in North America, owned by Berkshire Hathaway.

Headwinds

Economic Sensitivity: The rail industry is sensitive to economic cycles and changes in demand for goods.

Operational Challenges: Weather-related disruptions, labor strikes, and other operational challenges can impact performance.

Regulatory Environment: Stringent regulations can affect operations and profitability.

Volume Declines: Persistent softness in freight demand, as seen in recent quarters, challenges growth projections.

Labor and Costs: High fixed costs, unionized labor expenses, and fuel price volatility remain ongoing concerns.

Tailwinds

Technological Advancements: Investments in technology and digital solutions enhance efficiency and customer experience.

Environmental Sustainability: Rail transportation's lower carbon footprint makes it an attractive option for environmentally conscious customers.

Strategic Partnerships: Collaborations with other rail networks, trucking companies, and ports expand reach and capabilities.

Canadian National Railway (CNR)

Company Overview

Canadian National Railway Company (CNR) is a leading North American transportation and logistics company.

Founded in 1919 and headquartered in Montreal, Canada, CNR operates an extensive rail network spanning Canada and the United States. The company’s network stretches from the Atlantic to the Pacific coasts in Canada and extends south through the U.S. Midwest to the Gulf of Mexico.

The company provides rail services, intermodal services, trucking, and related transportation solutions. CNR serves various industries, including automotive, coal, fertilizers, forest products, grain, metals and minerals, petroleum and chemicals, consumer goods, and third-party logistics.

The company employs around 23,000 people and is publicly traded on the Toronto Stock Exchange (TSX: CNR) and New York Stock Exchange (NYSE: CNI).

Business Model

CNR’s business model revolves around providing efficient, reliable, and cost-effective freight transportation and logistics services across its extensive rail network. The company generates revenue primarily through freight transportation, leveraging its strategic infrastructure to move goods for various industries. Key elements of its business model include:

Freight Diversification: CNR transports a broad mix of commodities, including intermodal containers, petroleum and chemicals, grain and fertilizers, forest products, metals and minerals, automotive goods, and coal. This diversification helps mitigate risks associated with downturns in specific sectors.

Network Efficiency: CNR emphasizes operational excellence, optimizing its rail network to reduce transit times and costs while maximizing capacity. Investments in technology and infrastructure enhance its ability to handle high volumes of freight.

Ancillary Services: Beyond rail transport, CNR generates revenue through intermodal services (e.g., trucking and logistics), transloading, customs brokerage, and real estate leasing along its rail corridors.

Cost Management: The company balances high fixed costs (e.g., rail infrastructure maintenance) with variable costs (e.g., fuel and labor) by leveraging economies of scale and pursuing operational efficiencies.

CNR’s mission focuses on delivering value to customers and shareholders by maintaining a leadership position in North American transportation while adapting to economic and environmental trends, such as decarbonization efforts.

Product and Service Offerings

CNR provides a comprehensive suite of transportation and logistics services tailored to diverse customer needs:

Rail Services: Core freight transportation via rail, including equipment provision, private car storage, and custom brokerage for cross-border shipments.

Intermodal Services: Door-to-door solutions combining rail and trucking, with 23 strategically located terminals. Services include temperature-controlled cargo transport, port partnerships, and logistics park operations.

Trucking Services: Complementary offerings such as import/export drayage, interline services, and specialized trucking (e.g., flatbed and expedited cargo).

Supply Chain Solutions: End-to-end logistics support across industries, including automotive, agriculture, energy, and consumer goods.

Specialized Services: Handling of dimensional loads, overweight shipments, and tailored solutions for industries like coal, fertilizers, and forest products.

Sustainability Initiatives: Investments in hybrid diesel-battery electric locomotives (e.g., a recent purchase from Progress Rail in 2024) to reduce emissions and align with low-carbon goals.

In 2024, CNR’s revenue breakdown included intermodal (22%), petroleum and chemicals (20%), grain and fertilizers (20%), forest products (11%), metals and minerals (12%), automotive (5%), and coal (5%), with additional income from ancillary services.

Competitive Position and Advantages

Extensive Network: CNR’s coast-to-coast Canadian coverage and U.S. reach to the Gulf of Mexico provide unmatched market access, connecting major ports, industrial hubs, and agricultural regions.

Economic Moat: As part of a duopoly with Canadian Pacific Kansas City (CPKC) in Canada, CNR benefits from high barriers to entry, including the capital-intensive nature of rail infrastructure and regulatory hurdles.

Operational Efficiency: CNR’s focus on network optimization and technology (e.g., precision scheduled railroading) enhances service reliability and cost-effectiveness.

Financial Health: With a solid financial health score and a 29-year dividend growth streak, CNR demonstrates resilience and shareholder commitment.

Diversified Revenue: Exposure to multiple industries reduces reliance on any single sector, providing stability compared to competitors with narrower focus areas.

Canadian Pacific Railway (CP)

Company Overview

Canadian Pacific Railway (CP), now part of Canadian Pacific Kansas City (CPKC), is a Class I railway that operates a transcontinental freight railway in Canada and the United States.

Founded in 1881 and headquartered in Calgary, Alberta, CP has a rich history and has played a significant role in the development of Canada.

CPKC operates a vast network of approximately 20,000 route miles spanning Canada, the United States, and Mexico, making it the first and only single-line railway connecting these three countries.

CPKC employs around 20,000 people and serves as a critical artery for North American trade.

The company is publicly traded on the Toronto Stock Exchange (TSX: CP) and New York Stock Exchange (NYSE: CP).

Business Model

CPKC’s business model centers on providing efficient, reliable, and integrated freight transportation services across its expansive rail network. The company generates revenue through a combination of rail freight hauling and complementary logistics services, leveraging its unique transnational reach. Key components include:

Freight Transportation: CPKC transports a diverse range of goods, including bulk commodities (grain, coal, potash), merchandise freight (forest products, chemicals, automotive), and intermodal traffic (retail goods in containers). This diversification stabilizes revenue across economic cycles.

Single-Line Network: The merger with KCS enables seamless cross-border transport without interline handoffs, reducing transit times and costs for shippers moving goods between Canada, the U.S., and Mexico.

Operational Efficiency: CPKC employs precision scheduled railroading (PSR) principles to optimize train schedules, reduce dwell times, and improve asset utilization, driving profitability.

Ancillary Revenue Streams: The company offers intermodal trucking, logistics solutions, and real estate leasing along its rights-of-way, supplementing core rail income.

Capital Intensity: High fixed costs (infrastructure, rolling stock) are offset by economies of scale, with ongoing investments in technology and capacity to support long-term growth.

CPKC aims to capitalize on North American trade flows, particularly in the context of nearshoring and supply chain resilience, while maintaining a focus on sustainability and operational excellence.

Product and Service Offerings

Rail Freight Services: Core offerings include transportation of bulk commodities (e.g., grain, coal, fertilizers, sulphur), merchandise freight (e.g., energy products, chemicals, plastics, metals, forest products, automotive), and intermodal containers (retail goods).

Intermodal Solutions: CPKC operates a network of terminals (e.g., 23 key hubs) for seamless rail-to-truck transfers, including specialized services like the Mexico Midwest Express (MMX), offering 98-hour transit from Chicago to Monterrey/San Luis Potosí.

Cross-Border Services: Single-line haulage from Canada through the U.S. Midwest to Mexico, including intra-Mexico freight via concessions on over 3,000 miles of track.

Logistics and Supply Chain: End-to-end solutions, including transloading, customs brokerage, and port access (e.g., Vancouver, Atlantic Canada, Gulf of Mexico, Lázaro Cárdenas).

Specialized Equipment: Handling of oversized loads, temperature-controlled cargo, and automotive shipments.

Sustainability Initiatives: Development of hydrogen-powered locomotives (in collaboration with CSX) and fuel-efficient operations to meet environmental goals.

In 2024, revenue was driven by intermodal (25%), grain (20%), chemicals/plastics (15%), and automotive (10%), with other segments like coal and forest products rounding out the mix.

Competitive Position and Advantages

Unique Transnational Network: As the only single-line railway linking Canada, the U.S., and Mexico, CPKC offers unmatched connectivity, reducing reliance on interline agreements and enhancing speed/reliability.

Economic Moat: High barriers to entry (capital costs, regulatory approvals) and a near-duopoly with Canadian National Railway (CNR) in Canada protect CPKC from new entrants.

Strategic Merger Synergies: The KCS acquisition is projected to yield $1 billion+ in annual cost savings by 2026, boosting margins and operational scale.

Port Access: Connections to major ports across three countries position CPKC as a key player in global trade, particularly for intermodal growth.

Financial Stability: A 15-year dividend growth streak and a strong balance sheet (e.g., debt-to-equity manageable despite merger costs) appeal to investors.

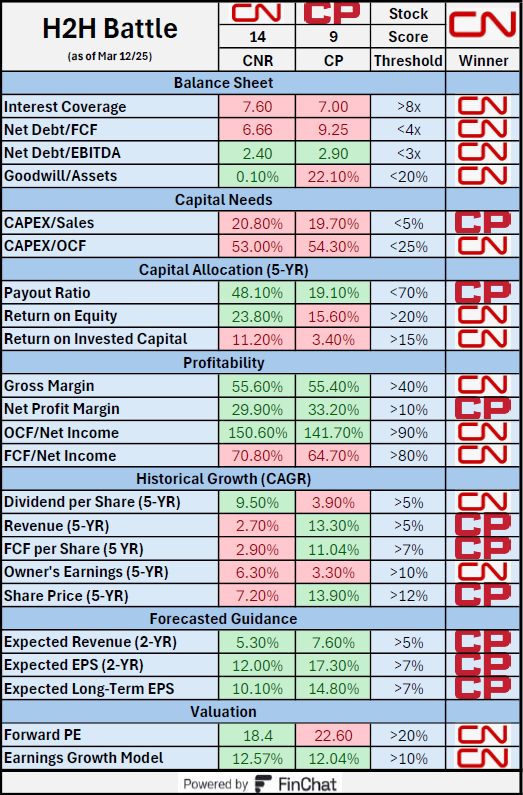

Outcome

Although it's not a clear-cut victory, CN (Canadian National Railway) edges out in this matchup of railroads. However, to an investor, each presents a distinct investment thesis. CN's emphasis on financial stability, cash flow quality, and value makes it a safer bet for conservative investors. On the other hand, CP (Canadian Pacific Railway) offers a compelling growth profile and higher forecasts, appealing to investors seeking upside potential.

Balance Sheet

In the transportation industry, particularly for railroads, balance sheets often carry significant debt due to high capital expenditures for infrastructure (tracks, trains, etc.). However, CN's lower leverage and minimal goodwill make it more resilient to economic downturns or asset write-downs, which are risks in capital-intensive industries. CP's higher Net Debt/EBITDA and goodwill may reflect its acquisitions (potentially explaining the goodwill and the taking on of more debt), increasing financial risk.

Capital Needs

Railroads require significant ongoing investment in maintenance and expansion, explaining the high CAPEX ratios. CP's slight advantage in CAPEX/Sales suggests it may be more efficient in generating revenue per dollar of capital spent, though both companies' high ratios indicate limited flexibility for other uses of cash. The high CAPEX/OCF for both suggests they are prioritizing growth or maintenance over immediate cash preservation, which could strain liquidity if cash flows decline.

Capital Allocation

CN's higher ROE and ROIC reflect stronger management efficiency in utilizing equity and invested capital to generate returns, a critical factor in a capital-intensive industry like railroads where assets (e.g., rail networks) are costly. CP's low payout ratio suggests a focus on retaining earnings, possibly for growth initiatives or deleveraging, but its lower ROE and ROIC indicate it’s less effective at turning capital into profits. CN strikes a better balance between rewarding shareholders and generating returns on capital.

Profitability

Railroads typically enjoy high gross margins due to their quasi-monopolistic market positions and economies of scale, which is reflected in both companies' figures. CP's higher net margin suggests better control over operating expenses or taxes, but CN's superior cash flow conversion (OCF and FCF relative to net income) indicates its earnings are more sustainable and less reliant on non-cash items. In this industry, cash flow metrics are crucial due to high capital expenditures, giving CN an edge in operational efficiency.

Historical Growth

CP's superior revenue and FCF per share growth suggest it has been more aggressive in expanding operations, possibly through acquisitions or market expansion, which aligns with its higher goodwill and debt levels. CN's slower growth in these areas may reflect a more conservative strategy, focusing on stability and dividend growth, which appeals to income-focused investors.

Forecasted Guidance

CP's higher forecasted growth in revenue and EPS suggests analysts expect it to continue its historical outperformance in scaling operations. This could be driven by strategic initiatives like network expansion, efficiency improvements, or favourable market conditions. CN's more modest forecasts still indicate growth but may reflect a more cautious outlook or a focus on profitability over aggressive expansion. In the railroad sector, growth forecasts can be influenced by economic conditions, trade volumes, and fuel prices, so CP's projections may assume stronger tailwinds.

Valuation

CN appears more attractively valued. Railroads often trade at premium valuations due to their stable cash flows and dividend yields, but CP's higher P/E indicates the market is assigning a growth premium, possibly due to its stronger historical and forecasted growth. CN's edge in the earnings growth model suggests it offers better value when balancing price with growth potential, making it more appealing for value-oriented investors.

Winner - CN Rail

Verdict - Split DecisionDisclaimer: The information provided is for educational and informational purposes only. It does not constitute financial advice or a recommendation to buy, sell, or hold any specific stocks or securities.

● Written with the help of Grok

Consider joining DiviStock Chronicles’ Referral Program for more neat rewards!

Get the H2H Battle Template for 3 successful referrals!Please refer to the details of the referral program.