Ending Quantitative Tightening (QT)

Why the Fed’s Quiet Pivot from Mortgage Bonds to T-Bills Could Reshape Liquidity, Rates, and Risk in 2026

Understanding the Federal Reserve’s monetary actions is essential for grasping broader economic implications. On October 29, 2025, the Fed announced it will end quantitative tightening (QT) starting December 1, 2025—a decision with potential consequences for the economy, financial markets, and interest rates. This article breaks down the mechanics of the move, adds contextual details, and explores possible underlying motives behind the Fed’s shift in strategy.

What’s Happening? The Fed’s Balance Sheet Shuffle

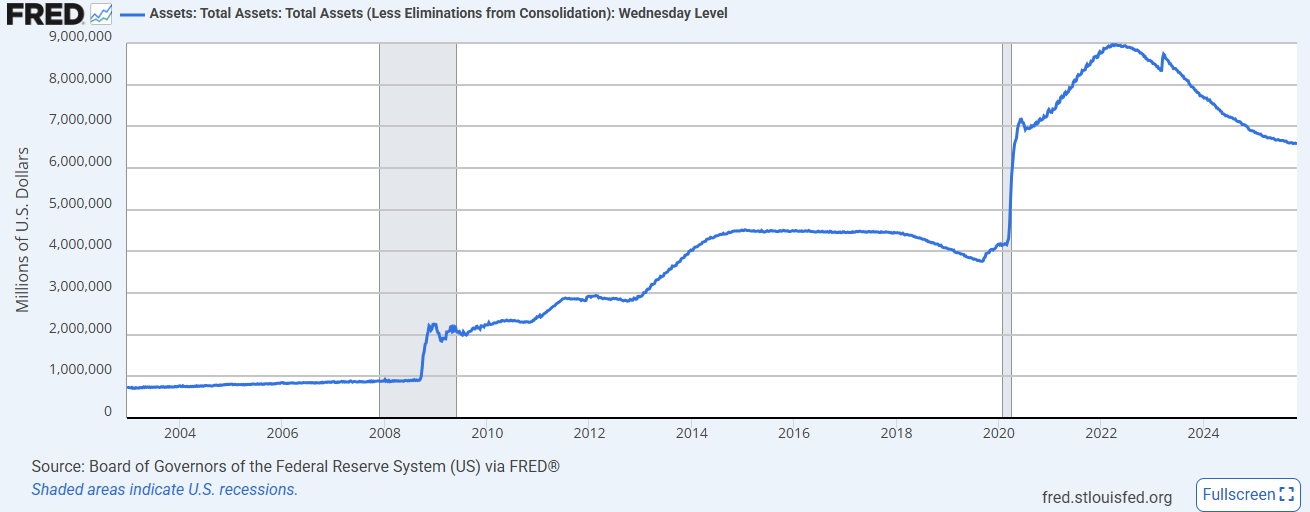

Think of the Fed as a giant bank managing a massive piggy bank for the U.S. economy. This piggy bank, known as the balance sheet, currently holds about $7 trillion in assets.

These assets include:

Mortgage-Backed Securities (MBS): Investments tied to home loans, totaling around $2.5 trillion as of late 2025.

Treasury Securities: Government debt, including short-term Treasury bills (T-bills) and longer-term notes/bonds, making up the rest (about $4.5 trillion).

For the past three years, the Fed has been shrinking this piggy bank through QT. It let assets mature—meaning when homeowners paid off mortgages or government debt came due—without always reinvesting the money, reducing the balance sheet from a peak of $8.9 trillion in 2022. Now, the Fed is hitting the pause button. Starting December 1, it will keep the balance sheet steady at $7 trillion instead of letting it shrink further. But it’s also reshuffling what’s inside—moving away from MBS and toward T-bills. Let’s dive into how this works!

How It Works: A Simple Example with Extra Detail

Let’s imagine the Fed’s $100 billion piggy bank (a smaller version of the real $7 trillion) is made up of:

$60 billion in MBS.

$40 billion in Treasuries (a mix of T-bills and longer-term bonds).

Each month, $10 billion of MBS matures as homeowners make payments or refinance their mortgages. During QT, this would be reinvested by the Fed and any excess run off to shrink the balance sheet. Now, under the new plan starting December 1, 2025, it will reinvest all $10 billion from maturing MBS—not into more MBS, but into short-term T-bills, which mature in 4 to 52 weeks and are seen as super-liquid (easy to turn into cash).

After One Month:

The $10 billion MBS matures, leaving $50 billion in MBS.

The Fed reinvests that $10 billion into new T-bills.

The piggy bank stays at $100 billion, now with $50 billion MBS and $50 billion Treasuries ($40 billion old + $10 billion new T-bills).

Next Month: Another $5 billion MBS matures (due to more homeowner payments). The Fed reinvests that into T-bills, leaving $45 billion MBS and $55 billion Treasuries—still $100 billion total.

This process lets MBS “roll off” naturally (shrink over time) while the Fed builds its T-bill holdings. The Fed buys these T-bills at Treasury auctions, placing non-competitive bids to ensure it gets a share, as outlined in the FOMC statement. This shift prioritizes short-term assets for flexibility, a key detail for understanding future moves.

Where Does the Money Come From? A Closer Look

When MBS or T-bills mature, the U.S. Treasury (the government’s financial arm) pays the Fed back. Here’s where that money originates with more detail:

Tax Revenue: The Treasury uses money collected from income taxes, corporate taxes, and other sources. For instance, if $10 billion in MBS matures, part might come from the $4–5 trillion in annual tax receipts.

New Borrowing: If taxes fall short, the Treasury borrows by issuing new T-bills, notes, or bonds. In 2025, the U.S. national debt is over $36 trillion, and the government borrows about $1–2 trillion yearly to cover deficits. For our $10 billion example, it might issue new T-bills, sold to investors like banks, foreign governments, or the Fed itself when reinvesting.

Fed’s Role: The Treasury pays the Fed from its account at the Fed, replenished by these sources. If the Fed reinvests (as it’s doing with MBS proceeds now), it uses that cash to buy new T-bills, keeping the balance sheet stable.

If the Fed ever lets T-bills roll off (not reinvesting when they mature), the balance sheet shrinks, and the Treasury must find other buyers for new debt—potentially raising interest rates if demand lags.

Why Is the Fed Doing This? Official Reasons and Critical Thinking

The Fed’s official explanation, per the October 29 FOMC statement1, is to maintain “liquidity” (ensuring cash flows smoothly in the banking system) and manage rising funding costs, as money market rates have tightened recently (noted by Reuters on October 29, 20252). The shift to T-bills, which are short-term and liquid, supports this by giving the Fed flexibility to handle unexpected needs. But let’s think critically—there could be deeper, less obvious reasons behind this move:

Preparing for Economic Trouble: The Fed might suspect a recession or financial crisis is brewing, even if it hasn’t said so publicly. The balance sheet drop from $8.9 trillion in 2022 to $7 trillion by late 2025 has reduced bank reserves from $3 trillion to under $2 trillion. Stopping QT now could be a safety net, with T-bills providing quick cash if banks or markets falter.

Critical question: Why act now unless data (e.g., loan defaults or corporate bond yields) hints at trouble?

Supporting Government Debt Under Pressure: With U.S. debt exceeding $36 trillion and deficits growing, the Treasury relies on low borrowing costs. Reinvesting MBS proceeds into T-bills keeps demand high, indirectly aiding the government. This could reflect political pressure, though the Fed denies it.

Critically, if the Fed were truly independent, why not let the balance sheet shrink further to signal tighter control, unless it’s bowing to fiscal needs?

Cooling a Potential Housing Bubble: MBS holdings have fallen from $2.7 trillion in 2022 to $2.5 trillion, and letting them shrink further might raise mortgage rates (e.g., from 6% to 6.5%), slowing a hot housing market. This could prevent a crash but avoid overt intervention.

Critical angle: Is the Fed avoiding blame for a housing correction, or does it see signs (e.g., rising home prices) that justify this gradual unwind?

Positioning for Future Rate Cuts: The Fed cut rates to 3.75%–4% on October 30, 2025, and T-bills’ short maturity lets it reinvest at lower rates if cuts continue in 2026. This could amplify easing without restarting full quantitative easing (QE).

Critically, why shift to short-term assets now unless the Fed anticipates needing to pivot quickly—possibly due to weakening job or inflation data?

Masking Banking Strain: The drop in reserves might signal stress in smaller banks, which rely on Fed liquidity. Stabilizing the balance sheet and favoring T-bills could quietly support them without a public bailout.

Critical thought: If this is true, why not disclose it—could it be to avoid panic or protect the Fed’s reputation?

These possibilities highlight the Fed’s balancing act. Its vague “operational reasons” leave room for speculation, so as an investor, stay skeptical and watch for clues in economic reports!

What Does This Mean for You? Practical Insights for Canadian Investors

As a Canadian value investor, dividend enthusiast, or long-term portfolio builder, the Fed’s actions south of the border can ripple into your investments. Here’s how this might affect you, considering your Canadian perspective:

Bond Investors: T-bills could keep U.S. short-term yields low (e.g., 4% vs. 5% for longer bonds), influencing Canadian bond yields since they often move in tandem (e.g., Canada’s 10-year bond yield at 3.5% as of October 2025). If you hold Canadian bonds or ETFs like VAB.TO, watch for potential rate alignment. Consider laddering.

Stock Market: A steady U.S. balance sheet might boost TSX stocks, especially those with U.S. exposure (e.g., banks like TD or energy firms like Enbridge). But recession fears could hit resource-heavy Canadian markets. Dividend stocks in stable sectors (e.g., utilities like Fortis at 4% yield) might offer resilience—check their U.S. revenue exposure.

Housing and Currency: Rising U.S. mortgage rates could strengthen the Canadian dollar (CAD) if capital flows shift, impacting your cross-border investments. For Canadian real estate investors, higher U.S. rates might cool demand, but Canadian mortgage rates (e.g., 5% variable) could also rise if the Bank of Canada follows suit. Monitor the CAD/USD exchange rate (around 1.38 as of October 27, 2025, per FRED).

Dividends: Liquidity support might help Canadian companies with U.S. ties pay dividends, but a U.S. slowdown could pressure payouts. Focus on firms with strong cash flow and low U.S. reliance.

Since Canada’s economy is tied to the U.S. (70% of exports go there), these Fed moves matter. Adjust your portfolio with this in mind!

Canada's Wake-Up Call

It only took one person to wake up the entire world, and now everyone is mad at him. Perhaps he is partially right; the reliance on America is so great that if a hindrance to that reliance emerges, these dependent economies could collapse. So, who is taking advantage of whom?

● Research supported by Grok, built by xAI.

Federal Reserve Board - Federal Reserve issues FOMC statement