Alimentation Couche-Tard - The Temporary Plateau of a High-Quality Business - FY24

As companies start to reveal their earnings for the fiscal year 2024, here are the results for a stock in my portfolio along with a business valuation.

Welcome to my summary of Alimentation Couche-Tard’s (ATD) earnings report for fiscal 2024. For additional context, please refer to my earlier post detailing my valuation methodology.

Year-End Results

Fuel will always be a volatile component of ATD's performance. Through disciplined cost control, the company has managed to offset the persistent high inflation pressures. This company has made the pullback in consumer spending apparent. The impact of this trend is likely to be evident in the earnings reports of many businesses over the next few quarters, not just ATD. A major activity in fiscal 2024 was the expansion of the European network, marked by the acquisition of 2,175 sites from TotalEnergies SE.

Revenues saw a 4% decrease.

Earnings per share (EPS) decreased by 8%, with adjusted EPS down by 10%.

Dividends per share (DPS) increased by 25%.

Operating cash flow (OCF) was $4.8 billion, and free cash flow1 (FCF) was $2.8 billion.

The payout ratio stood at 24%.

The long-term debt to equity ratio was 0.98.

The average share price growth was 17% over 5 years, 20% over 3 years, and 24% over the last year.

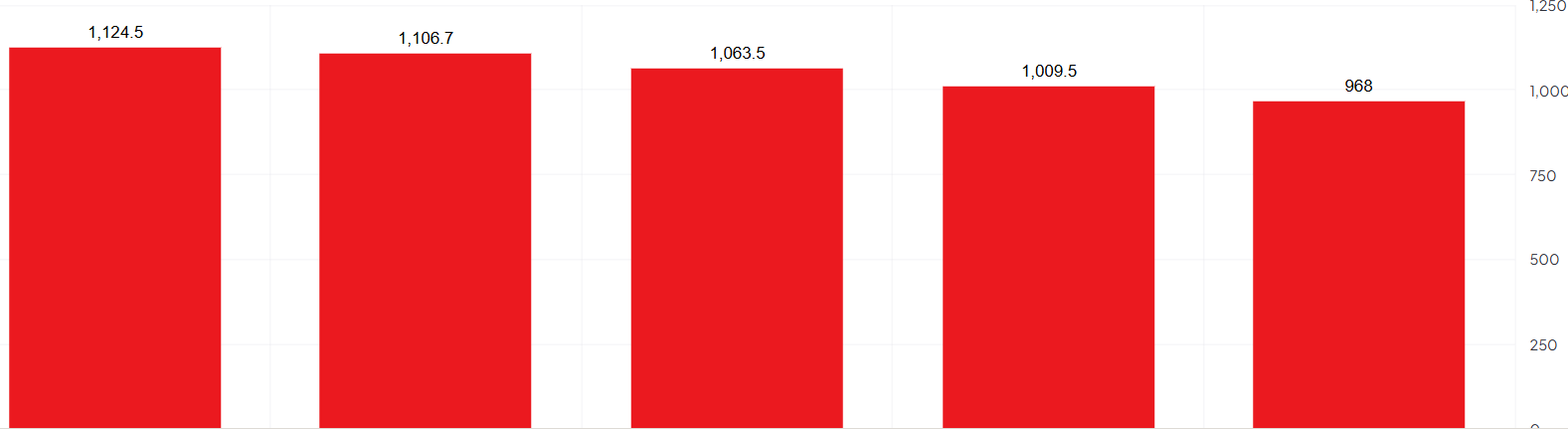

The count of outstanding shares continued to decrease.

ATD’s weighted average shares outstanding for past five years

Investor Presentation Highlights

The company has broadened its geographic diversity through recent acquisitions in Europe, yet revenue is still predominantly derived from fuel sales. Nonetheless, profit margins are split between fuel and merchandise/services.

The US market remains highly fragmented, presenting opportunities for ATD to expand its footprint within the country.

ATD's growth strategy primarily depends on acquisitions to propel growth, yet risks arise from integration challenges and the potential for overpaying for assets. History is on its side though.

Future ambitions. With a strong balance sheet and cash flows steadily growing, this creates ample opportunity for ATD to continue its merger and acquisitions strategy for the foreseeable future, even amid tighter financial constraints.

What about the Electrical Vehicle Transition?

Fossil fuels are anticipated to maintain their dominance in the vehicle sector for the foreseeable future. The adoption of electric vehicles (EVs) is encountering growing challenges, including the escalating costs of materials and the financial investment needed to develop EV infrastructure.

Nonetheless, ATD has established a presence in the European market, particularly in Scandinavian countries, where the adoption of electric vehicles is significantly higher.

The debt maturity schedule is well-balanced, featuring a weighted average term to maturity of eleven years.

Leadership change. Brian Hannasch announced his retirement as President and CEO, with Alex Miller appointed as the next President and CEO effective September 6.

Alex Miller has a substantial background in the retail fuel and convenience store industry, with over 25 years of management experience. He joined Alimentation Couche-Tard in 2012. Prior to his tenure at Couche-Tard, Miller worked for BP for 16 years.

Not every successor yields positive results. Although Hannasch's retirement is not optimal, considering his contributions to the company's growth, he will remain involved as a special advisor in the short term, concentrating on mergers and acquisitions.

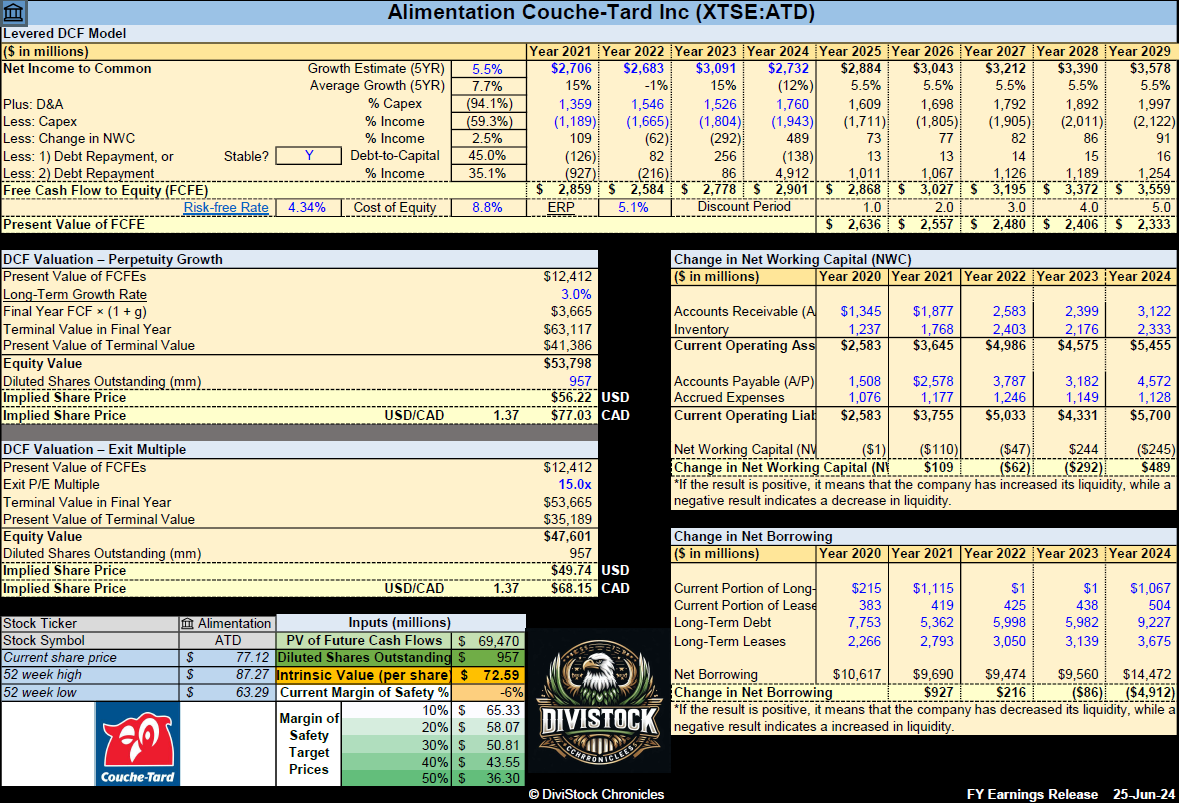

My Own Valuation

Despite the challenges of price inflation, reduced fuel margins, and other macroeconomic factors, ATD continues to hold a strong competitive edge due to effective expense management, strategic acquisitions, and a disciplined approach to mergers and acquisitions.

It seems that the short-term growth has already been accounted for in the current price. Pullbacks are rare and infrequent. Despite the underperformance in the previous two quarters, there has yet to be a significant pullback.