Brookfield Infrastructure Partners - Growth is Promising - FY24

As companies start to reveal their earnings for the fiscal year 2024, here are the results for a stock in my portfolio along with a business valuation.

Welcome to my summary of Brookfield Infrastructure Partners’ ($BIP.UN/$BIPC) earnings report for fiscal 2024. For additional context, please refer to my earlier post detailing my valuation methodology.

Year-End Results

Brookfield Infrastructure Partners (BIP) continues its impressive growth as a company, but stock price still lags. As part of the Brookfield group, it stands to benefit from the US's emphasis on energy initiatives moving forward.

Revenues increased by 17%.

Adjusted EPS increased by 11%.

Funds from Operations1 (FFO) increased by 6%.

Dividends, or distributions, per share (DPS) increased by 6%.

The payout ratio remained around 67%, which is within the company's target range of 60%-70%.

Operating cash flow (OCF) was $4.6 billion, and adjusted funds from operations2 (AFFO) was approximately $1.8 billion.

Total debt has increased, but the proportionate net debt to capitalization (based on market value) remains around 50%. AFFO to total debt ratio decreased slightly to 3.64.

The annualized average growth rate of the share price was +4% over five years, -3% over three years, and -2% over the past year.

The number of outstanding shares has marginally risen.

Investor Call Highlights

FFO Growth in All Areas on a comparable basis.

Utilities: Generated FFO of $760 million, up 7% year-over-year.

Transport: FFO was $1.2 billion, a 40% increase from the prior year.

Midstream: FFO of $625 million, reflecting an 11% growth.

Data: FFO of $333 million, a 21% increase over the prior year.

FFO stands for Funds From Operations. It's a key financial metric used primarily by real estate investment trusts (REITs) and other income-producing properties. FFO measures the cash generated by a company's operations, excluding the effects of depreciation and amortization, which are non-cash expenses. This metric provides a clearer picture of a company's operating performance and its ability to generate cash flow from its core business activities.

Unprecedented Capital Recycling Program. BIP achieved $2 billion in capital recycling proceeds in 2024 and has already secured $200 million in proceeds from asset sales in early 2025. They expect to deliver $5-6 billion in asset sale proceeds over the next two years.

Inflation? No problem! BIP is well-positioned to benefit from higher inflation. Their businesses provide essential services with regulated or contracted revenue streams (~90%), many of which are indexed to inflation. Additionally, BIP has managed its capital structures to mitigate interest rate risks.

Steady Payout Ratios. BIP has demonstrated exceptional management of payout ratios. In addition to fostering growth, their payout distributions have been a pleasant accretion. BIP has successfully achieved its target payout ratio of 60-70% of funds from operations while increasing its distribution by an average of 7%.

Data Center Hype. Data centers are one of the most significant areas of investment with over $3.6 billion of capital invested in the last 6 years alone. DeepSeek has brought questions around the magnitude of hardware, servers, power, and data centres needed. However, BIP remains positive about long-term data center demand growth.

My Own Valuation

Reading through BIP’s financials is an interesting read. The dynamics of how to evaluate the business really need to be understood. The diversification that the company offers is highly attractive, from utilities to transport to data centres. It is a universal hit!

The debt levels may seem alarming, but it is necessary for what BIP is. Regardless, it is important to note that the majority of their borrowings are nonrecourse.

Non-recourse borrowing is a type of loan where the borrower is not personally liable beyond the collateral specified in the loan agreement. Essentially, if the borrower defaults on the loan, the lender can only seize the collateral and cannot go after the borrower's other assets or income. This is in contrast to recourse borrowing, where the lender can pursue additional assets or legal action to recover the remaining debt after the collateral is sold.

This type of borrowing is common in project financing and commercial real estate transactions, where the loan is secured by the property or project itself. Non-recourse loans can offer significant benefits to borrowers by limiting their risk, but they often come with higher interest rates and stricter terms to offset the increased risk for lenders. Keeping an eye on this is important, but as long as AFFO is increasing as well, BIP should be relatively safe.

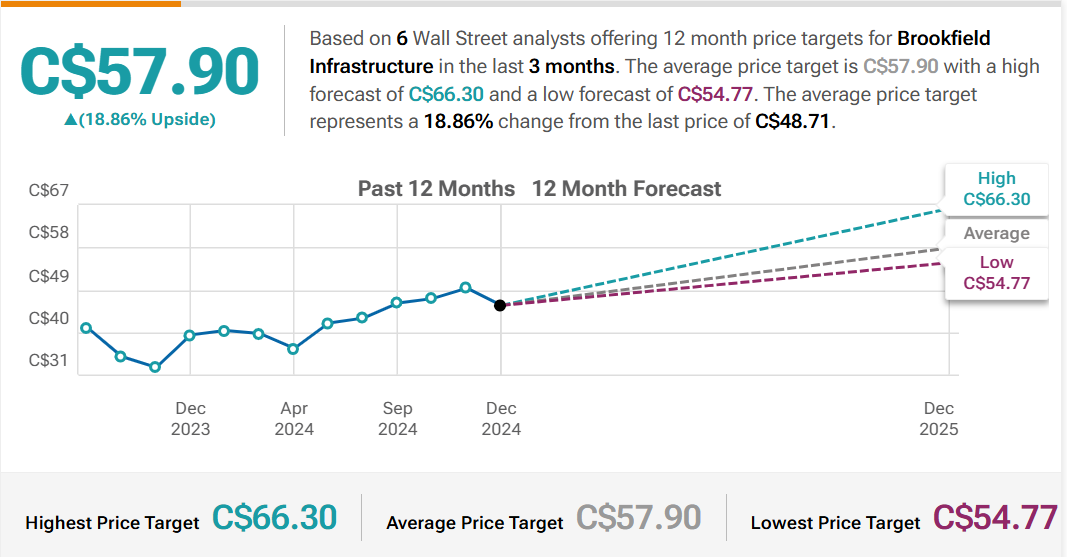

From a market perspective, it has been out of favour for a very long time ever since its all-time highs. Although a bit of a speculative play, the growth it offers going forward is appealing. The price is now coming up as the market is slightly realizing its potential.

Net Income Growth: The spreadsheet presents a growth estimate that reflects the company's anticipated rise in net income for the upcoming five years, based on the average of projections from multiple analysts. The estimate is additionally adjusted down to reflect a more conservative approach.

Free Cash Flow to Equity (FCFE): This is calculated for several years, showing the amount of cash that could be distributed to shareholders after all expenses, reinvestment, and debt repayments.

Discounted Cash Flow (DCF) Valuation: The spreadsheet includes a DCF valuation section, which is a method used to estimate the value of an investment based on its expected future cash flows. It provides two valuation methods:

Perpetuity Growth: Calculated using a long-term growth rate and discounting future cash flows.

Exit Multiple: Based on an exit price-to-earnings (P/E) multiple.

Current Share Price vs. DCF Value: A table compares the current share price of ATD with the estimated share price based on DCF valuation, suggesting whether the stock is undervalued or overvalued according to the model.

Disclaimer: The information provided in this valuation analysis is for educational and informational purposes only. It does not constitute financial advice or a recommendation to buy, sell, or hold any specific stocks or securities. The valuation model presented here relies on certain assumptions, including projected future cash flows and discount rates.

Other FY24 Reviews

Consider joining DiviStock Chronicles’ Referral Program for more neat rewards!Please refer to the details of the referral program.