BCE Inc. - Oy Vey - FY24

As companies start to reveal their earnings for the fiscal year 2024, here are the results for a stock on my watchlist along with a business valuation.

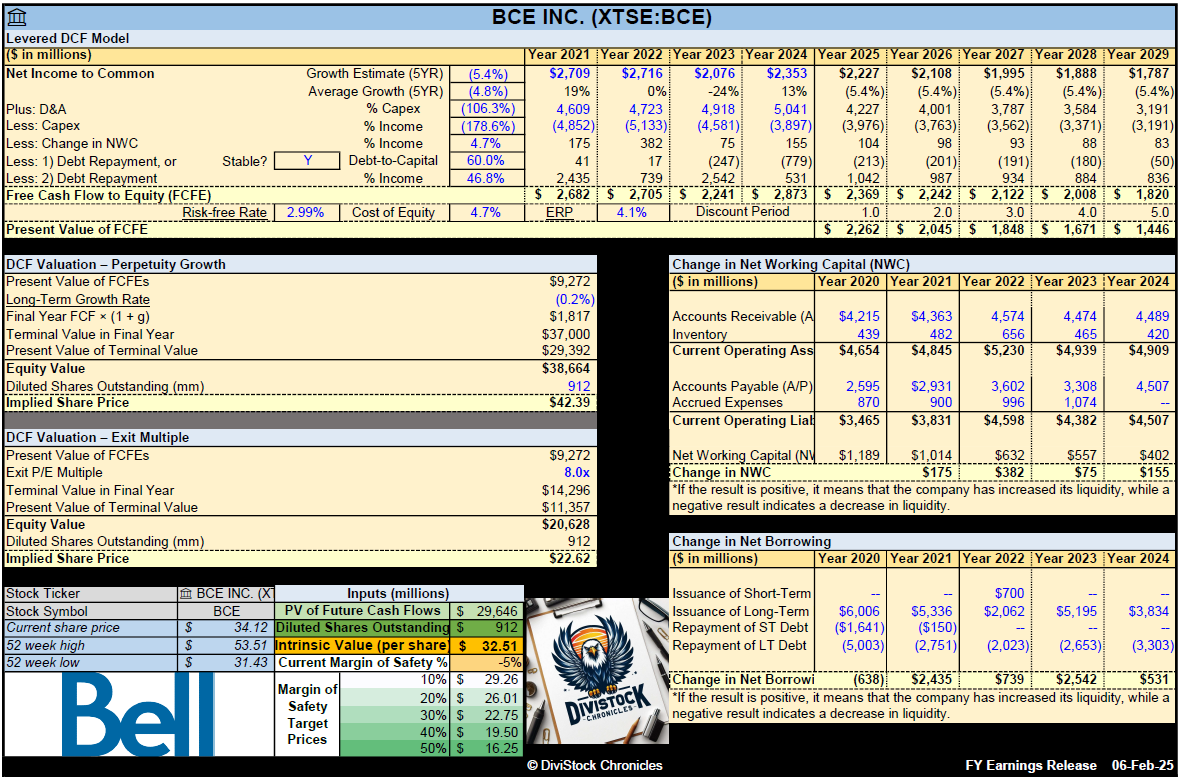

Welcome to my summary of Bell’s ($BCE) earnings report for fiscal 2024. For additional context, please refer to my earlier post detailing my valuation methodology.

Year-End Results

So, what positives can we take from BCE’s fiscal year performance for 2024? Absolutely nothing!

Revenues decreased by 1%.

Earnings per share (EPS) experienced a large 92% decrease, while the adjusted EPS decreased by 5%. Mainly related to Bell Media’s TV and radio properties that reflected a further decline in demand and spending in the traditional advertising market.

I've previously discussed the challenges faced by traditional media companies, especially in today's landscape with the multitude of new avenues for media services.

Dividends per share (DPS) increased by 3%.

The payout ratio on a free cash flow basis closed at approximately 126%, marking the highest it has ever been. This significantly exceeds BCE’s previous payout targets of 65%-75%.

Operating cash flow (OCF) declined to $7 billion, and free cash flow1 (FCF) followed at approximately $2.8 billion.

The net profit margin dropped to 1.5%.

The long-term debt-to-equity ratio pushed to more elevated levels at 1.93 with a FCF to Debt of 0.07. Trouble has been brewing for a while now.

The annualized average growth rate of the share price was -5% over five years, -9% over three years, and -21% over the past year.

The number of outstanding shares is materially unchanged.

Investor Call Highlights

Ziply Acquisition. I've previously expressed how absurd this decision appears at first glance. Refer to my previous publication, which prompted me to fully offload my BCE shares. The MLSE net sale proceeds of approximately $4.2 billion, initially intended for debt repayment, are now being directed towards the acquisition of Ziply Fiber. But here’s the quick, they are open to building out the Ziply fiber footprint with help of third-party capital to reduce funding requirements. This tells me that entered this market due to this potential opportunity…

BCE Outlook - Is it a Sinking Ship?

There has been a concerning downtrend in Bell Canada (BCE) ever since the all-time highs in April of 2022. Amidst rising interest rates, the company's growth has been stifled by its substantial debt. Additionally, limited revenue expansion due to increased competition and disappointing performance in other divisional segments has compounded the issue.

Dividend. Management acknowledges the very unhealthy payout ratio that exceeds BCE’s policy range. While they did not discuss increasing or cutting the dividend during the conference call, their slides indicate a plan to maintain the same dividend amount in 2024, with no increase! If you are a dividend GROWTH investor, this is a final sign that it is time to move on.

Capex to Slow Down. We saw a great reduction in capital expenditures (capex) this past year as a result of the slowdown of BCE’s fiber build in Canada. This is as a result of a regulatory decision that provided Telus and other large carriers temporary wholesale tariff access to BCE’s fiber network.

BCE management is confused on why a regulator would put in place policies that create disincentives to investment, puts jobs at risks and puts at risk the building out of critical infrastructure.

In other words, if this decision is reversed, expect capex to creep up again.

My Own Valuation

I commend you if you're sticking with BCE, or if you see this as an upside entry point. While the yield is attractive to many, others view it as a sign of a potential dividend cut. Historically, when companies reduce dividends, stock prices tend to fall further. How long can BCE sustain this high dividend yield?

Given the oligopolistic nature of the industry in Canada, I understand the appeal of these companies. However, with the slowdown in immigration, tighter consumer budgets, and the shift from traditional media to streaming services, traditional telecommunications companies like BCE face significant challenges. Additionally, BCE's debt load is concerning. Comparing it to Verizon (VZ) in the U.S., Verizon's annualized EPS growth has been less than ideal.

Long-term, if BCE manages to survive its debt burden, it has the potential to recover nicely. However, the wait might be lengthy. A dividend cut could have mixed implications: on the positive side, it would allow BCE to address its debt more effectively with its consistent cash flows. On the negative side, the stock price would likely drop further. Nonetheless, such a scenario might present a very intriguing entry point for me.

After owning and subsequently selling off BCE, it is no longer on my watchlist. I am completely moving on from this company, unless management can turn the ship around and manage their debt levels more carefully. My only telecommunications exposure now is to Telus, which is in somewhat better shape, but still not stellar.

Net Income Growth: The spreadsheet presents a growth estimate that reflects the company's anticipated rise in net income for the upcoming five years, based on the average of projections from multiple analysts. The estimate is additionally adjusted down to reflect a more conservative approach.

Free Cash Flow to Equity (FCFE): This is calculated for several years, showing the amount of cash that could be distributed to shareholders after all expenses, reinvestment, and debt repayments.

Discounted Cash Flow (DCF) Valuation: The spreadsheet includes a DCF valuation section, which is a method used to estimate the value of an investment based on its expected future cash flows. It provides two valuation methods:

Perpetuity Growth: Calculated using a long-term growth rate and discounting future cash flows.

Exit Multiple: Based on an exit price-to-earnings (P/E) multiple.

Current Share Price vs. DCF Value: A table compares the current share price of ATD with the estimated share price based on DCF valuation, suggesting whether the stock is undervalued or overvalued according to the model.

Disclaimer: The information provided in this valuation analysis is for educational and informational purposes only. It does not constitute financial advice or a recommendation to buy, sell, or hold any specific stocks or securities. The valuation model presented here relies on certain assumptions, including projected future cash flows and discount rates.

Other FY24 Reviews

Alphabet Inc. - Waiting on AI Breakthrough - FY24

Welcome to my summary of Alphabet’s ($GOOG/$GOOGL) earnings report for fiscal 2024. For additional context, please refer to my earlier post detailing my valuation methodology.

Consider joining DiviStock Chronicles’ Referral Program for more neat rewards!Please refer to the details of the referral program.